Market Sentiment Surrounding Texas Pacific Land (TPL)

The market is talking about Texas Pacific Land (TPL) as its recent share price performance has drawn significant attention. Currently priced at US$502.85, TPL has experienced remarkable momentum, with a 30-day share price return of 44.94% and a 90-day gain of 74.52%.

Despite this impressive performance, analysts are questioning whether the stock still holds value or if its future growth is already priced in. Notably, the most popular narrative suggests that TPL is approximately 79.1% overvalued, with a fair value estimated closer to US$280.83.

Valuation Concerns

Market expectations are tempered by anticipated declines in high-yield Permian reserves and the maturation of production across TPL’s acreage, which could lead to lower royalty volumes. These factors may challenge the optimistic revenue and free cash flow assumptions currently reflected in the stock’s valuation.

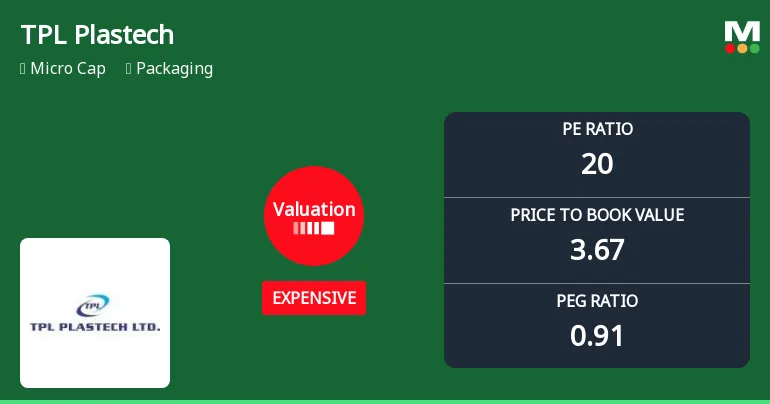

Furthermore, TPL Plastech’s P/E ratio of 20.03 indicates a shift from fair to expensive valuation, suggesting that the market is pricing in robust earnings expectations. With a price-to-book value ratio of 3.67, TPL is trading at a premium compared to its net asset value.

Comparative Analysis

When compared to industry peers, TPL’s valuation appears elevated but not excessively so. For instance, Apollo Pipes trades at a P/E of 44.52, while Rajoo Engineers is at 18.25. This comparative context illustrates that while TPL may seem expensive, it is in line with market expectations for growth and profitability.

Conclusion

As the market continues to analyze Texas Pacific Land’s position, investors are advised to proceed with caution. No official confirmation yet on future performance metrics, but the current valuation dynamics suggest a complex landscape ahead.